Fordecades, pharmaceutical M&A followed a familiar rhythm: identify apromising late-stage asset, pay a premium, integrate it into the portfolio.That model is being displaced.

Over the past year,a clear pattern has emerged. Leading manufacturers are no longer simplyshopping for molecules, instead systematically acquiring capabilities - AIdiscovery platforms, drug delivery technology, manufacturing control points - thatexpand opportunities across multiple assets. In effect, the focus has shiftedfrom buying the harvest to owning the orchard.

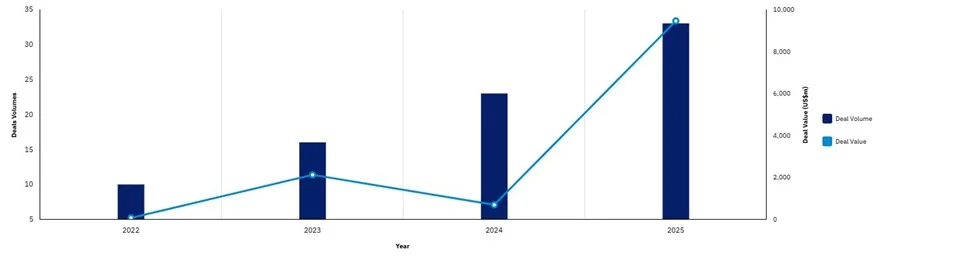

Themost visible shift toward capability-buying is in AI. Since 2022, M&A dealsinvolving artificial intelligence have increased in volume and valuesignificantly (Fig. 1), as leading companies embed AI within their existing infrastructure,particularly in drug discovery and development.

To expand their early pipeline, many large manufacturers areturning to partnerships with AI-native technology companies. Merck KGaArecently expanded its collaboration with Valo Health to use AI and patientdatasets within a research engine focused primarily on discovering newtreatments for Parkinson’s disease.1 This partnership pairs Merck’srobust drug development capabilities with a human causal biology platformcomprised of patient records and biobank samples to identify specific patientphenotypes and new target points for therapeutic intervention. BoehringerIngelheim’s collaboration with Variant Bio follows the same logic.2While kidney disease is the entry point, the asset is population-scale geneticdata paired with an AI discovery system that can be redeployed as prioritiesshift to reduce the time required to move from genetic association to validatedtherapeutic hypothesis.

Companies are also investing in platforms, from deliverymechanisms to new modalities, that can be translated across assets, particularlywhere control of underlying technology creates durable advantage.

Eli Lilly's obesity partnerships, including NimbusTherapeutics, are structured around oral and metabolic platforms, not singleassets. Notably, this latest partnership focuses on an oral modality fortraditionally injectable obesity treatments, overcoming a significant barrierfor multiple assets in the heavily competitive space.6

Capability buying is not limited to R&D. Manufacturingand supply chain control are increasingly viewed as strategic assets, shaped bygeopolitics, trade policy, and speed requirements.

As tariffs have increased the cost of internationalmanufacturing and supply chains, some large manufacturers are bolstering theirend-to-end domestic footprint. Samsung Biologics' acquisition of GSK'sRockville facility establishes its first U.S. manufacturing footprint,providing faster client access and reinforcing capacity as competitiveadvantage.8 Moderna's decision to onshore fill–finish manufacturingcompletes its end-to-end domestic mRNA network, giving it full value chaincontrol and compressing development-to-commercial timelines.9

These moves reveal common logic:across discovery, modality development, and manufacturing, leading companiesare choosing repeatable systems over individual outputs.

The risk of inaction is subtle butsignificant. Companies that continue to rely primarily on late-stage assetacquisition may find themselves paying more for less differentiation, whilecompetitors quietly build engines that outlearn and outscale them.

The defining strategic question is nolonger “What should we buy next?” but “What capabilities do we want to still beusing five programs from now?”[MB1]

Get expert analysis, industry trends, and exclusive updates delivered straight to your inbox. Stay ahead of the curve with valuable insights that drive success.