Facing a sharp revenue decline after Entresto lost U.S. exclusivity in July, Novartishas moved aggressively to restock its pipeline, highlighted by a $12B acquisition ofAvidity Biosciences. The deal brings a novel platform for antibody-targeted RNAtherapeutics and an advanced Duchenne muscular dystrophy program with an FDAdecision anticipated in late 2025. This move follows additional neuroscience andcardiometabolic expansions, including the purchase of Tourmaline Bio's Phase IIasset pacibekitug and new RNA-based partnerships with Arrowhead and Argo.

With semaglutide set to lose patent protection in India in March2026, the GLP-1 landscape is preparing for substantial genericentries, with multiple domestic manufacturers readying low-costformulations expected to price at a fraction of the originator.Anticipating this shift, Novo Nordisk has implemented pricereductions of up to 37% for Wegovy, materially lowering monthlytherapy costs in a market where affordability will stronglyinfluence treatment uptake. The adjustment positions Novo toretain share during a period of heightened price sensitivity andsignals an effort to recalibrate expectations ahead of astructurally lower post-exclusivity pricing environment.

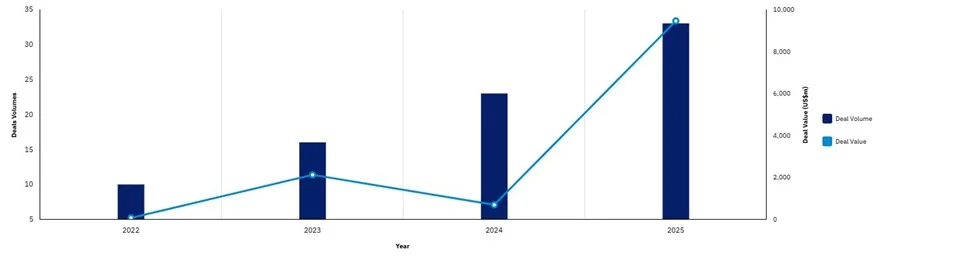

FDA Commissioner Marty Makary recently proposed treating biosimilars morelike generics, accepting analytical comparability and dropping most "switching"trials, which could halve development time, save up to $100 million per productand lower prices by up to 90% as early as 2026. At the same time, officials saythe U.S. Patent and Trademark Office (USPTO) is working to effectivelycounteract these policies by denying most inter partes review (IPR) requestswith stricter rules, and contributing to a "patent thicket" that makes challenges10-20x more expensive than in Europe, delaying market entry for biosimilars.

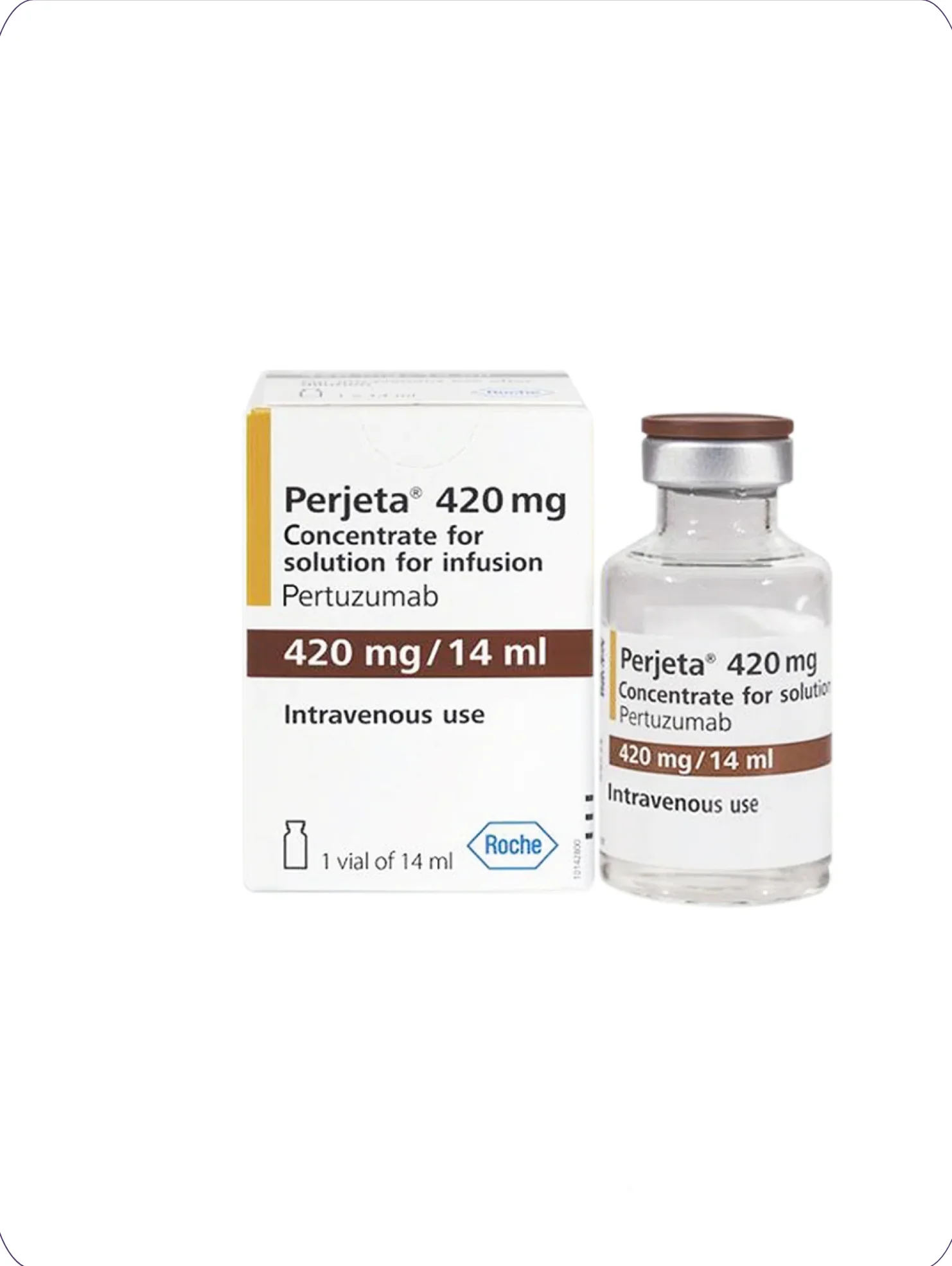

The FDA recently approved Poherdy as an interchangeable biosimilar to Roche'sPerjeta for all existing HER2-positive breast cancer indications, shortly afterPerjeta's primary patents expired and as Roche continues shifting patients to itsfixed-dose Phesgo combination. Perjeta revenue has already declined 13percent year over year in the first nine months of 2025, and additionalpertuzumab biosimilars are advancing as the FDA pursues policies intended toreduce development costs for future entrants.

Merck recently announced a nearly $9.2 billion acquisition of Cidara Therapeutics,adding CD388, a long-acting, strain-agnostic antiviral now in a 6,000-patientPhase III trial designed to prevent influenza infection in high-risk individuals.CD388, which holds FDA Breakthrough and Fast Track designations, previouslydemonstrated a 76 percent reduction in symptomatic influenza over 24 weeks in amid-stage study and aims to provide season-long protection in a single dose. Thedeal follows a string of acquisitions as the company prepares for late-decade lossof exclusivity for Keytruda, including the ~$10B purchase of Verona Pharma for itsfirst-in-class COPD therapy and ~$11.5B purchase of cardiopulmonary therapymanufacturer Acceleron Pharma.

Regeneron recently settled its patent litigation with Celltrion, clearing the wayfor the launch of another Eylea biosimilar in 2026. The agreement voids afederal court injunction from July 2024 and follows a similar settlement withSandoz, marking the second resolution in recent months as the FDA hasalready approved five Eylea biosimilars, including Amgen's first-to-marketproduct. These developments arrive as Regeneron's Eylea franchise, whichgenerated $5.97 billion in revenue last year, faces declining performance, withQ2 sales down 25% year over year.

Get expert analysis, industry trends, and exclusive updates delivered straight to your inbox. Stay ahead of the curve with valuable insights that drive success.